Bittensor Ecosystem Deep Dive: How the Network Actually Works

You’ve heard the Bittensor rally. But most people who hold TAO still can’t answer: why does this architecture actually produce value? This is that answer.

Most TAO holders understand the narrative.

Decentralized AI + Subnets competing for emissions + Jensen Huang mentioned it + Grayscale filed an ETF

What most people still haven’t worked through is the mechanics underneath, how emissions actually flow, what makes an Alpha token worth holding vs. a trap, why Taoflow wasn’t a minor upgrade but a complete restructuring of incentives, and what the subnet data actually tells you about where value is accumulating.

That’s what this piece is.

If you already hold TAO or are actively evaluating subnet positions, this is the framework I use to think about the network.

Here’s what we’re covering:

The Architecture: What TAO Actually Coordinates

Why “decentralized AI” undersells the design

The three-layer structure (base layer → subnets → Alpha tokens)

Subnet Mechanics: How Incentives Are Wired

Miners, validators, and why the scoring game matters

The Alpha AMM: price mechanics and what moves it

Where most people misread Alpha token risk

Taoflow: Why November 2025 Changed Everything

The exploit Taoflow killed

Net staking flow as the real signal

How to read flow data to spot momentum early

The Halving’s Second-Order Effect

Supply math isn’t the interesting part

Emission concentration and what it means for capital allocation

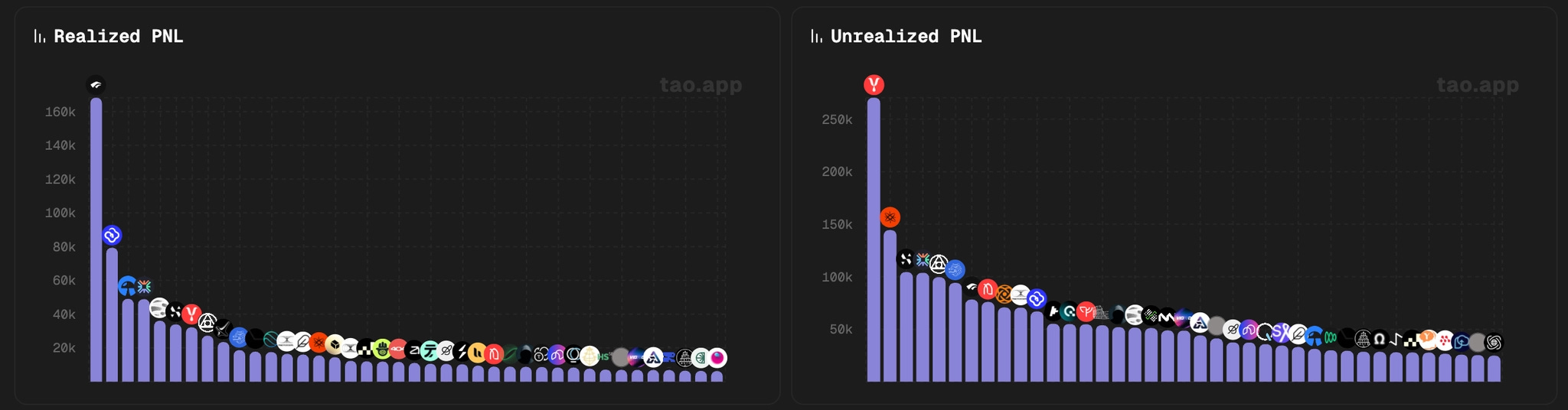

Reading the Subnet Leaderboard

What emission share, rPnL, and staking velocity actually tell you

Chutes, Targon, Templar - what each one proves

TAO vs. Alpha: A Framework for Positioning

When TAO is the right bet

When an Alpha position makes sense (and when it doesn’t)

Let’s get into it.

The Architecture: What TAO Actually Coordinates

The standard framing: “Bittensor is a decentralized AI network” is technically correct and analytically useless.

Here’s the more useful framing: Bittensor is a capital allocation protocol for AI compute.

TAO’s job is not to power AI inference directly. Its job is to route capital, via emissions and staking - toward the AI compute providers, trainers, and infrastructure builders that the market decides are most valuable.

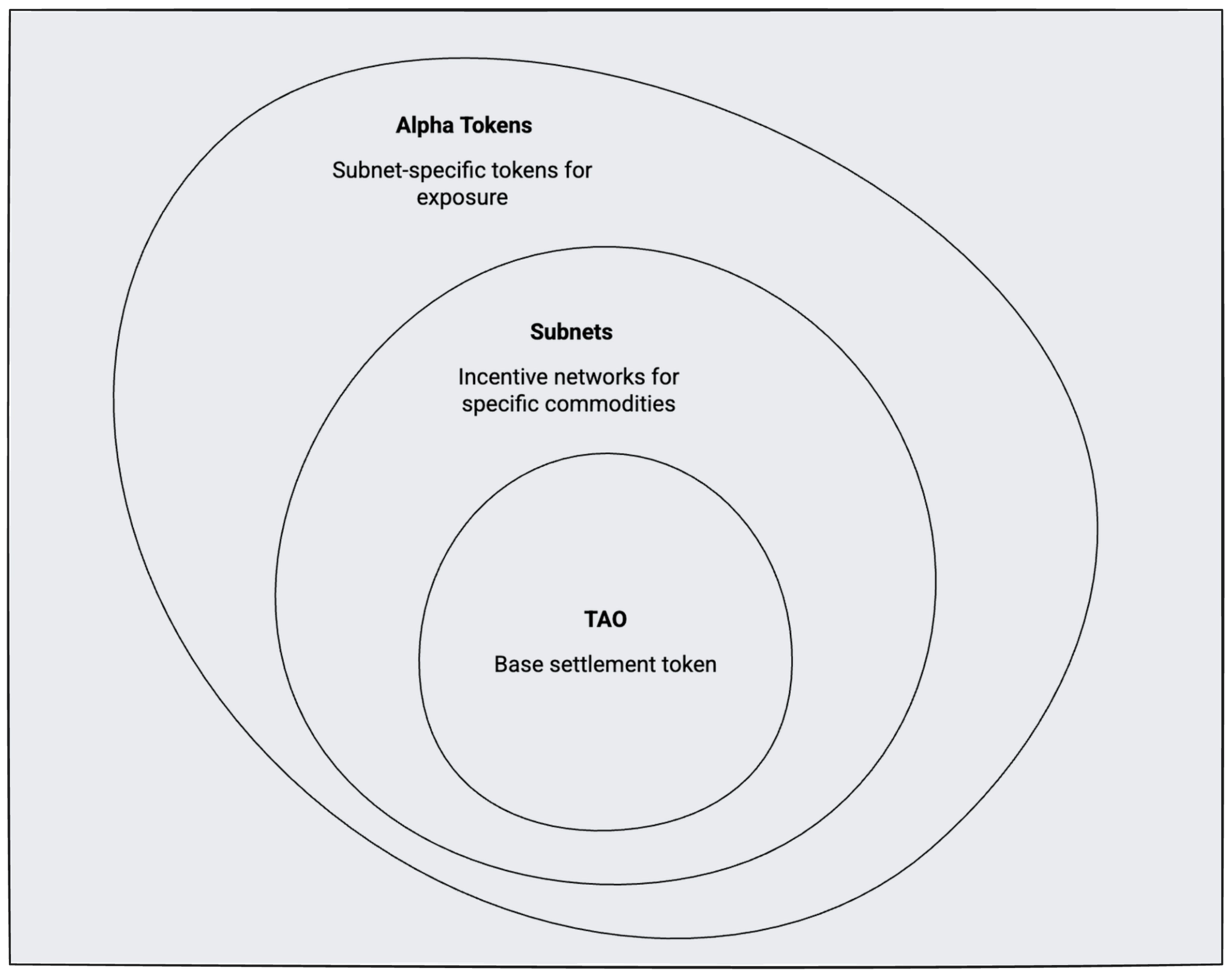

✨ The three layers:

Layer 1 - TAO (the base layer): The settlement token. Used for staking, emission distribution, and cross-subnet capital flows. Every subnet’s value is ultimately denominated in TAO.

Layer 2 - Subnets: Individual incentive networks, each producing a specific digital commodity. A subnet is an incentive structure that rewards whoever produces the best version of a specific output (inference quality, training throughput, data freshness, etc.).

Layer 3 - Alpha tokens: Subnet-specific tokens created when TAO is staked into a subnet’s AMM pool. These are the actual position-taking instruments for concentrated subnet exposure.

TAO doesn’t capture value from subnets directly. It captures value from the demand to stake TAO into subnets. The more capital that wants exposure to subnet Alpha tokens, the more TAO gets locked into pools, reducing circulating supply and increasing scarcity.

Subnet Mechanics: How Incentives Are Wired

The scoring game

Every subnet runs a continuous competition. Miners produce outputs (serve inference, train model weights, process data). Validators score those outputs against a benchmark. High-scoring miners receive more emissions. Low-scoring miners get nothing and eventually get de-registered.

This matters for two reasons:

Validator quality determines subnet quality. A subnet with lazy validators will drift toward gaming the benchmark rather than producing real value. When evaluating a subnet, look at how validators are scoring, not just the miner output metrics.

The benchmark design is the subnet’s moat. Subnets with hard-to-game benchmarks (like Chutes’ actual inference throughput measured against real queries) attract more credible miners. Subnets with soft benchmarks get gamed within weeks.

The Alpha AMM: what actually moves price

When you stake TAO into a subnet, it enters an on-chain AMM pool. You receive Alpha tokens proportional to your share of the TAO side of the pool.

Alpha tokens have a hard supply cap of 21 million and auto-compound emissions every ~72 minutes (one “tempo” = 360 blocks).

What actually moves Alpha price:

Net TAO inflow → TAO pool grows → Alpha price rises (denominated in TAO)

TAO price appreciation → your Alpha position is worth more in USD even if the TAO/Alpha ratio is flat

Emissions concentration → top subnets receive disproportionate emissions, compounding their liquidity advantage

Where most people misread Alpha risk:

Alpha tokens carry no formal revenue claim. What you hold is a token whose value is determined entirely by (a) staking inflow dynamics and (b) whatever the market decides to price in about the subnet’s future.

This means Alpha tokens in subnets with negative staking flow can go to zero quickly and under Taoflow, negative flow also means zero emissions, removing the one mechanism that was buffering value.

My take: Alpha tokens are closer to prediction market positions on subnet adoption than they are to equity. Price them accordingly. The expected value is asymmetric but so is the wipeout probability.

Taoflow: Why November 2025 Changed Everything

Before Taoflow, emissions were allocated based on subnet token price relative to TAO.

This created a straightforward exploit:

Coordinate a price pump in your subnet’s Alpha token

Capture a large share of emissions at the inflated price

Use emissions to build a TAO treasury

Slowly liquidate while continuing to collect rewards

Subnets could extract significant value from the protocol without producing anything real. Stakers following the emission signal were effectively subsidizing teams that had learned to game the metric.

Taoflow replaced price with net staking flow, TAO staked in minus TAO unstaked out, smoothed over a 30-day half-life EMA.

The implications:

Zero net flow = zero emissions. There’s no floor. A subnet that stops attracting capital stops receiving protocol subsidy.

The signal is real money moving, not price. You can’t fake staking inflow without actually deploying capital. The manipulation cost went from “coordinate a few wallets” to “put real TAO at risk.”

Flow momentum compounds. A subnet with consistent positive flow builds a larger pool → lower slippage → more attractive entry for larger capital → more flow. The rich get richer, but only if they’re actually shipping.

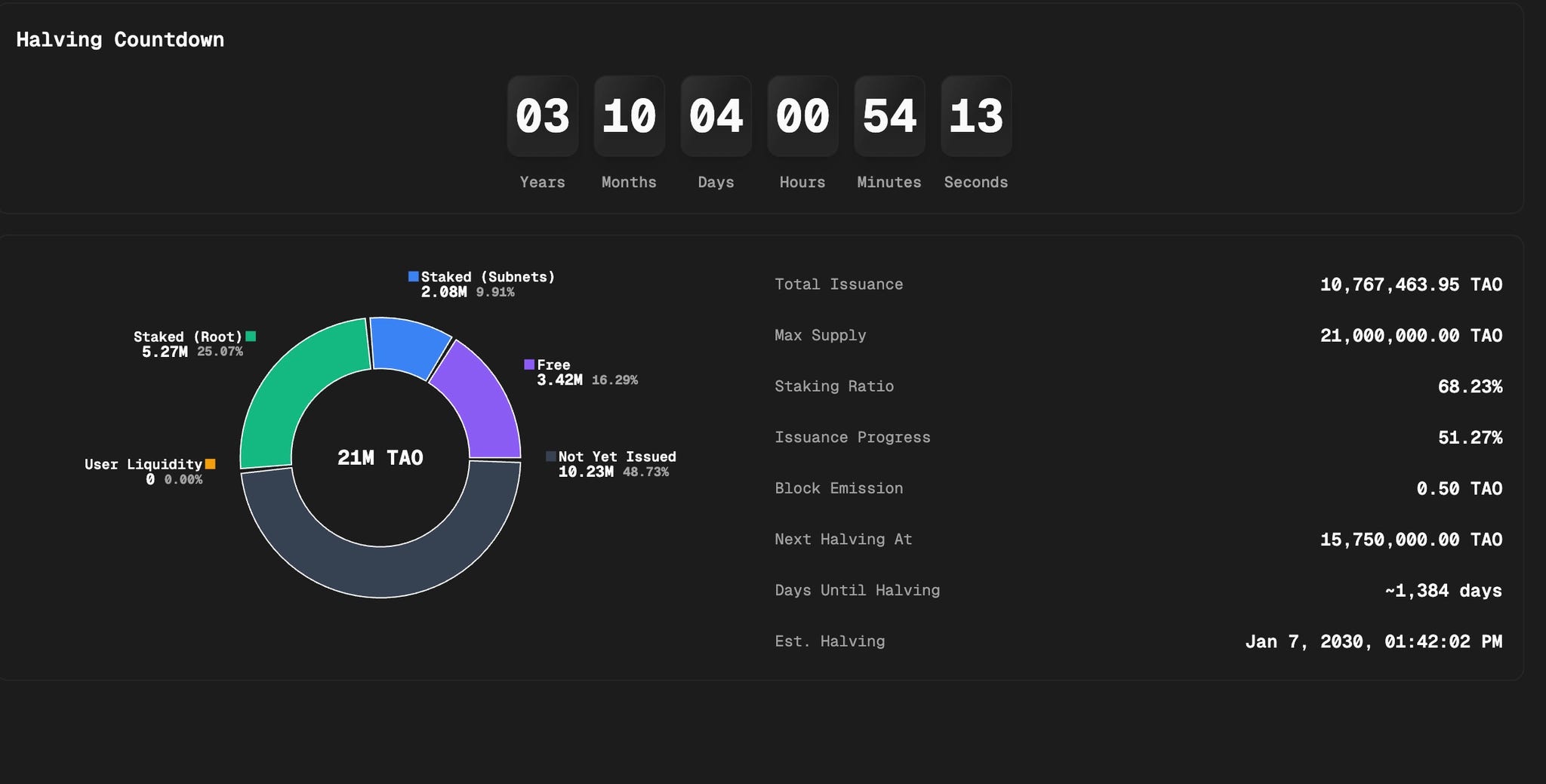

The Halving’s Second-Order Effect

The surface-level halving story: daily emissions dropped from 7,200 to ~3,600 TAO on December 14, 2025. Less new supply = Bullish.

But the more interesting effect is what the halving did to emission concentration.

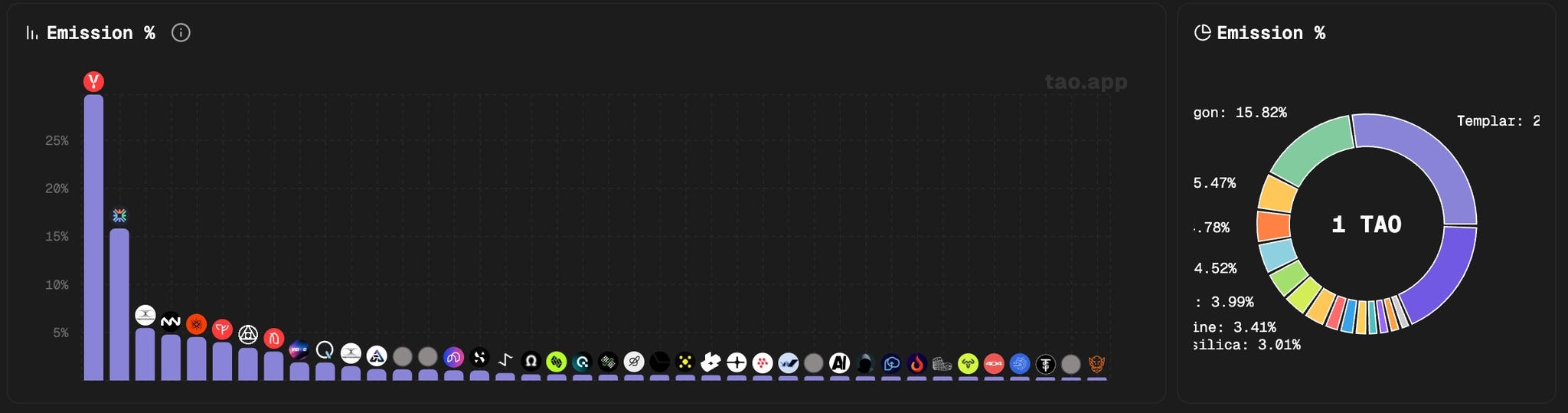

With fewer total emissions being distributed, the gap between top and bottom subnets widened. The top 10 subnets now capture ~56% of ~3,600 TAO/day. The remaining 118 subnets split ~44%.

For the bottom half of subnets, the post-halving environment is existential. With smaller absolute emission numbers and the same TAO staking threshold required to maintain positive flow, marginal subnets are being forced to either find product-market fit fast or wind down.

What this means for capital allocation:

The halving didn’t just make TAO scarcer. It concentrated the network’s value accrual into fewer, stronger subnets. The spread between a top-5 subnet Alpha position and a bottom-50 position is now wider than it’s ever been.

Reading the Subnet Leaderboard

Three metrics that actually matter when evaluating subnets:

Emission share: what percentage of daily TAO does this subnet capture? Top 10 control ~56%. Anything below 1% is fighting for survival.

Realized Alpha PnL (rPnL): the actual USD or TAO value extracted by stakers who entered and exited. This is the only metric that confirms the flywheel worked for capital, not just the team. A subnet with high emission share but low rPnL may be capturing emissions but not generating exit liquidity.

Staking velocity: how quickly is new TAO flowing in? High velocity with rising Alpha price = momentum. High velocity with flat/falling price = the pool is absorbing sells from early holders.

What the top three subnets prove

Chutes (SN64): Proof that product-market fit maps to staking inflow. 400k users. 9.1T tokens processed. 85% cheaper than AWS. Revenue auto-staked back into the pool. In February 2026, attracted +2,740 TAO in 9 hours on a single demand spike. This is what the flywheel looks like when it’s working.

Targon (SN4): Proof that AI inference is a real business on this network. $10.5M annual revenue. ~10.4% emission share. $12.47M in realized PnL for stakers. The number that matters: rPnL exceeds $10M ARR, meaning stakers captured more than one full year of revenue equivalent in exit value.

Templar (SN3): Proof of a different claim: that frontier-scale LLM training is feasible without centralized infrastructure. Covenant-72B was trained across 70+ global contributors on commodity hardware, confirmed in a March 2026 arXiv paper.

Currently captures ~30% of all daily emissions - the largest single share. The bull case is asymmetric: at ~$100M market cap, you’re pricing in almost nothing about what happens if decentralized training becomes the standard for open-source frontier models.

TAO vs. Alpha: A Framework for Positioning

These are genuinely different instruments with different risk profiles. Using the same framework for both is a mistake.

TAO = network-level exposure

You capture the aggregate growth of the ecosystem without needing to identify individual winners. The halving makes supply math favorable. Institutional access is expanding (Grayscale ETF filing, Virtune ETPs on Nasdaq Stockholm). Correlation to AI narrative cycles means TAO benefits from sector momentum even when specific subnets underperform.

The cost: your upside is capped by network growth, not individual subnet breakouts. A subnet going 10x in Alpha doesn’t move TAO proportionally.

Right for: long-term conviction on decentralized AI infrastructure, without the bandwidth to actively monitor subnet flow data.

Alpha tokens = concentrated startup bets

When you buy Alpha, you’re making a specific claim: this subnet will attract more capital than the market currently prices in. The return profile is startup-like - mostly zeros, occasional 10–100x.

The mechanics that determine whether an Alpha position works:

Does the subnet have a hard-to-game benchmark? (Sustainability)

Is net staking flow positive and accelerating? (Momentum)

Is rPnL positive for recent entrants? (Liquidity health)

Does the subnet have external revenue that feeds back into the pool? (Organic demand)

My recommendation: Default to TAO for network exposure. Move into Alpha positions only when you’ve done the subnet-specific due diligence. The best Alpha entry is when positive flow is just starting to accelerate and the Alpha/TAO price ratio hasn’t repriced yet.

The tools:

taostats.io for flow and emission data.

taomarketcap.com for subnet valuation comparisons

tao.app for explore TAO eco